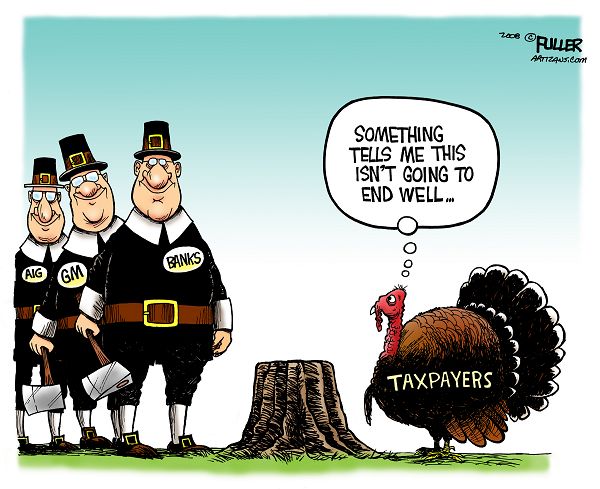

BANKSTER BAILOUT

WHERE THE

WALL STREET BAILOUT IS GOING:

“The

New Trough”

By Naomi Klein

Preface by Christopher Rudy, Editor of “Beware

and Prepare News”:

Beware of “bailout solutions” that compound the same corruption that is

bankrupting the economy and currency of conscience. Heaven knows that the trend

trajectory of greed and crony capitalism is unsustainable. For us to expect

different results -- while leaders maintain the same worth-ship of mammon

and militarism above all – is a good definition of insanity. Obviously, there

will be no definitive solutions with the same consciousness that created the

core systemic problems afflicting the Republic. Common sense may be uncommon in

these volatile times – suppressed as it is by the imbedded corporate media – but

the better part of valor now requires it. Dare to prepare for come what may! ~

CR

"Those who

profess to favor freedom, and yet depreciate agitation, are men who want crops

without plowing up the ground. They want rain without thunder and lightning.

They want the ocean without the awful roar of its waters. This struggle may be a

moral one; or it may be a physical one; or it may be both moral and physical;

but it must be a struggle! Power concedes nothing without a demand. It never

did, and it never will.

Find out just what people will submit to, and you have found out the exact

amount of injustice and wrong which will be imposed upon them; and

these will continue until they are resisted with either words or blows, or with

both.

The limits of tyrants are prescribed by the endurance of those whom they

oppress."

-

Thomas Paine, Common Sense, 1776

--------- article follows:

WHERE THE

WALL STREET BAILOUT IS GOING:

“The

New Trough”

The Wall

Street bailout looks a lot like Iraq a "free-fraud zone" where

private contractors cash in on the mess they helped create.

By NAOMI

KLEIN, Posted Nov 13, 2008

EXCERPT:

In Iraq, the contractors were tasked with reconstructing the country from

the mess made by U.S. missiles. After years of corruption born of no-bid

contracts and paltry oversight, many Iraqis are still waiting for the lights to

come back on. Today, a new team of contractors is lining up to reconstruct the

U.S. economy reconstruct it from the mess made by the very banks, brokers and

law firms that are now applying for contracts. And it's not at all clear that

America can survive their assistance.

Editor's note: The online version of this story at

http://www.rollingstone.com/politics/story/24012700/the_new_trough has been

amended to reflect developments since the publication of the print edition.

On October 13th, when the U.S. Treasury Department announced the team of

"seasoned financial veterans" that will be handling the $700 billion bailout of

Wall Street, one name jumped out: Reuben Jeffery III, who was initially tapped

to serve as chief investment officer for the massive new program.

On the surface, Jeffery looks like a classic Bush appointment. Like Treasury

Secretary Henry Paulson, he's an alum of Goldman Sachs, having worked on Wall

Street for 18 years. And as chairman of the Commodity Futures Trading Commission

from 2005 to 2007, he proudly advocated "flexibility" in regulation a

laissez-faire approach that failed to rein in the high-risk trading at the heart

of the meltdown.

Bankers watching bankers, regulators who don't believe in regulating that's all

standard fare for the Bush crew. What's most striking about Jeffery's

résumé

however, is an item omitted when his new job was announced: He served as

executive director of Paul Bremer's infamous Coalition Provisional Authority in

Baghdad, during the early days of the Iraq War. Part of his job was to hire

civilian staff, which made him an integral part of the partisan machine that

filled the Green Zone with Young Republicans, investment bankers and Dick Cheney

interns. Qualifications weren't a big issue back then, because the staff's main

function was to hand over stacks of taxpayer money to private contractors, who

were the ones actually running the occupation. It was this nonstop cash conveyor

belt that earned the Green Zone a reputation, in the words of one CPA official,

as "a free-fraud zone." During Senate hearings last year, when Jeffery was asked

what he had learned from his experience at the CPA, he said he thought that

contracts should be handed out with more "speed and flexibility" the same

philosophy he cited back when he was in charge of regulating Wall Street

traders.

The Bush Administration has since reversed the Jeffery appointment, perhaps

thinking better of giving a CPA alum such a central role in the Wall Street

bailout. Still the original impulse underscores the many worrying parallels

between the administration's approach to the financial crisis and its approach

to the Iraq War. Under cover of an emergency, Treasury is rapidly turning into

an economic Green Zone, overrun with private companies collecting lucrative

contracts. Fittingly, one of the first to line up at the new trough was none

other than the law firm of Bracewell & Giuliani yes, that Giuliani. The firm's

chairman, Patrick Oxford, could scarcely conceal his glee over the prospect of

cashing in on the bailout. "This one," he told reporters, "is very, very big."

At least four times bigger, in fact, than the post-9/11 homeland- security

bubble, from which Giuliani and his various outfits have profited so

extravagantly. Even bigger, potentially, than the price tag for the Iraq War

itself.

In Iraq, the contractors were tasked with reconstructing the country from the

mess made by U.S. missiles. After years of corruption born of no-bid contracts

and paltry oversight, many Iraqis are still waiting for the lights to come back

on. Today, a new team of contractors is lining up to reconstruct the U.S.

economy reconstruct it from the mess made by the very banks, brokers and law

firms that are now applying for contracts. And it's not at all clear that

America can survive their assistance.

See if any of this sounds familiar:

As soon as the

bailout was announced, it became clear that Treasury officials would hire

outsiders to perform their jobs for them at a profit. Private companies wanting

to help manage the bailout were given just two days to apply for massive,

multiyear contracts. Since it was such a mad rush after all, the entire economy

was about to implode there was no time for an open bidding process. Nor was

there time to draft rigorous rules to make sure that those applying don't have

serious conflicts of interest. Instead, applicants were asked to disclose their

conflicts and to explain and this is not a joke their "philosophy in fulfilling

your duty to the Treasury and the U.S. taxpayer in light of your proprietary

interests and those of other clients." In other words, an open invitation to

bullshit about how much they love their country and how they can be trusted to

regulate themselves.

[emphasis added ~CR]

The first major contract to be awarded in the bailout was for legal advice and

the choice Treasury made was Halliburton-esque in its audacity. Six law firms

were invited to bid, but four declined, either because they didn't want the

contract or because they had too many conflicts of interest. Rep. Barney Frank,

chairman of the House Financial Services Committee, said the fact that so many

law firms chose not to bid "shows that the guidelines are sufficiently

rigorous."

Or it may just show that the bidder who won the contract Simpson Thacher &

Bartlett takes a more relaxed approach to conflicts than its colleagues. The law

firm is a Wall Street heavy hitter, having brokered some of the biggest bank

mergers in recent years. It also provided legal support to companies trading

mortgage-backed securities the "financial weapons of mass destruction," as

Warren Buffett called them, that detonated the banking industry. More to the

point, it was hired to provide legal services to the Treasury in its

negotiations to spend $250 billion of the bailout money purchasing equity in

America's banks. The first stage of the plan involves buying stakes in nine of

the country's top banks. Incredibly, Simpson Thacher has represented seven of

the nine: JPMorgan, Bank of New York Mellon, Bank of America, Citigroup, Morgan

Stanley, Goldman Sachs and Merrill Lynch.

According to its contract, Simpson Thacher has agreed not to represent any of

the banks "against the U.S." when they negotiate with Treasury for the equity

money. However, the firm has retained the right to represent banks when they

apply for other parts of the $700 billion bailout not covered by its contract.

(It has promised to erect a "firewall" to stem the flow of "confidential

information" to those clients.) The firm will also continue to work for the

banks on a range of other lucrative deals and that's where the problem lies.

Take Lee Meyerson, Simpson Thacher's lead lawyer on the bailout negotiations,

who is specifically named in the contract as "essential" to the project. As the

company's hotshot attorney, Meyerson has personally represented three of the

nine banks that were bailed out in the first round, in addition to many others

that will surely apply for cash injections. One of the bailed-out banks is Bank

of New York Mellon, whose $29 billion merger Meyerson helped negotiate. Mergers

like that can bill in the millions. Is Simpson Thacher able to put aside its

loyalties to its biggest clients and negotiate deals for the taxpayer that could

exact real costs from those very clients?

It might be possible to set aside concerns about divided loyalties if it were

clear that Simpson Thacher is helping Treasury to wrangle the best deals

possible for U.S. taxpayers. But the firm's first test the deal to give $125

billion to the nine big banks to ease the "credit crunch" that is crippling the

economy wasn't exactly reassuring. Secretary Paulson promised that the banks

won't just "hoard" the money they will quickly "deploy it" through the economy

in the form of badly needed loans. There is just one hitch: Neither Paulson nor

Simpson Thacher got that "deploy" part in writing nor did they put in place any

mechanism to require the banks to spend their taxpayer billions. Apparently, the

part about lending the money to homeowners and small businesses was sort of

implied.

"There is no obligation for banks to lend the money one way or the other,"

Jennifer Zuccarelli, a Treasury spokeswoman, tells Rolling Stone. "But the banks

have the understanding" that the money is intended for loans. "We're not looking

to control their operations."

Unfortunately, many of the banks appear to have no intention of wasting the

money on loans. "At least for the next quarter, it's just going to be a

cushion," said John Thain, the chief executive of Merrill Lynch. Gary

Crittenden, chief financial officer of Citigroup, had an even better idea: He

hinted that his company would use its share of the cash $25 billion to buy up

competitors and swell even bigger. The handout, he told analysts, "does present

the possibility of taking advantage of opportunities that might otherwise be

closed to us."

And the folks at Morgan Stanley? They're planning to pay themselves $10.7

billion this year, much of it in bonuses almost exactly the amount they are

receiving in the first phase of the bailout. "You can imagine the devilish grins

on the faces of Morgan Stanley employees," writes Bloomberg columnist Jonathan

Weil. "Not only did we, the taxpayers, save their company...we funded their 2008

bonus pool."

It didn't have to be this way. Five days before Paulson struck his deal with the

banks, British Prime Minister Gordon Brown negotiated a similar bailout only he

extracted meaningful guarantees for taxpayers: voting rights at the banks, seats

on their boards, 12 percent in annual dividend payments to the government, a

suspension of dividend payments to shareholders, restrictions on executive

bonuses, and a legal requirement that the banks lend money to homeowners and

small businesses.

In sharp contrast, this is what U.S. taxpayers received: no controlling

interest, no voting rights, no seats on the bank boards and just five percent in

dividend payouts to the government, while shareholders continue to collect

billions in dividends every quarter. What's more, golden parachutes and bonuses

already promised by the banks will still be paid out to executives all before

taxpayers are paid back.

No wonder it took just one hour for Paulson to convince all nine CEOs to accept

his offer less than seven minutes per bank. Not even the firms' own lawyers

could have drafted a sweeter deal.

The day after it met with the nation's top banks, Treasury announced that it had

selected the firm that would receive the juiciest contract of all: that of

"master custodian." The winning company will be to the bailout what Halliburton

is to the military: the contractor of contractors. It will purchase toxic debts

from Wall Street, service them and auction them off in the future a so- called

"end-to-end process." The contract is for a minimum of three years.

Seventy firms applied for the gig; the winner was Bank of New York Mellon.

Describing the scope of the megacontract, bank president Gerald Hassell said,

"It's the ultimate outsourcing because the Federal Reserve and the Treasury do

not have the mechanics to run the entire program, and we're essentially the

general contractor across the entire program. It's going to cross our entire

company."

This raises an interesting point: Has the Treasury partially nationalized the

private banks, as we have been told? Or is it the other way around? Is it

Treasury that has been partially privatized by Wall Street, its massive rescue

plan now entirely in the hands of a private bank it is directly subsidizing?

Shortly after receiving the contract, Hassell told investors that his

institution is now well-positioned to profit from the market meltdown. "There's

a lot of new business that's going on even in this chaotic marketplace," he

said, "and so some of those things have been very positive to us." Just how

positive, we don't know, because Treasury has blacked out the 10 lines of the

"master custodian" contract that reveal how much Bank of New York Mellon will be

paid. Though Treasury says it will release the information eventually, the

secrecy goes beyond anything the Bush administration attempted in Iraq. Even

Halliburton's dodgy contracts came with price tags attached.

Still, when the terms of the contract do become public, they may turn out to be

surprisingly modest. Goldman Sachs has apparently offered to fulfill at least

one bailout contract for free. Altruism may not be their only motivation. The

real money at stake in the bailout lies not in payment for the work but in how

the work is done. Think about it: If you're the one selling your debts to the

government, wouldn't you also want to help decide which debts are eligible and

how much they're worth? "The financial firms with assets to sell are in many

instances the same firms the Treasury will rely on to value and manage the

assets it is buying," The New York Times observed. "That is an invitation for

these firms to set the price too high or to indulge in other mischief at the

taxpayers' expense."

Bank of New York Mellon has a bad record for mischief. It is embroiled in a

$22.5 billion money-laundering lawsuit in Moscow and has been forced to pay out

a $14 million settlement in a related case. Though the bank's "master custodian"

contract with Treasury prohibits unethical conduct, the arrangement seems rife

with opportunities for abuse. According to its most recent earnings report, Bank

of New York Mellon holds $1.2 billion in subprime mortgage securities. That

means that in addition to the $3 billion it will receive as part of the equity

program, it will also be eligible to apply for taxpayer money from the program

it is being paid to administer. Neither the bank nor Treasury would comment on

this direct conflict of interest.

On the same day that he allocated the first $125 billion to the banks, Secretary

Paulson announced the largest federal budget deficit in U.S. history. Buried in

his statement was a preview of the next phase of the financial disaster. The

deficit numbers, he declared, reinforce the need to "pursue policies that

promote economic growth and fiscal responsibility, and address entitlement

reform." He was referring to Americans who feel entitled to receive Social

Security in their old age and Medicaid when they are sick. Those programs,

Paulson implied, might not be able to survive the budget crisis he is currently

creating for the next administration.

This is why the stakes of the bailout are so high: Unless we get a good deal,

there will be nothing left over after the banks are done feeding to pay for the

meager services now provided in exchange for taxation, let alone for the more

ambitious initiatives promised on the campaign trail. The spiraling cost of

saving Wall Street from its bad bets is already being used as an excuse for why

we can't solve our many other crises, from health care to climate change.

There is a better way to fix a broken financial system. Treasury's plan to buy

up the toxic debts never made sense and should be immediately scrapped -- a move

that would also handily get rid of most of the crony contractors. As for

purchasing equity in banks, the next round of deals and there will be more has

to start from the premise that the banks are bankrupt and will therefore accept

whatever terms we choose to impose, including real regulatory oversight. The

possibilities of what could be done if a chunk of the banking system were

genuinely under public control from a moratorium on home foreclosures to

mandatory investment in green community redevelopment are limitless.

Because here is what George Bush and Henry Paulson are hoping we won't figure

out:

When a

society no longer has enough money to pay for its most pressing needs,

there are worse things than discovering you own the banks.

[Or is

that the Big Illusion in this confidence game… that the Federal Reserve

Bank is “Federal” when in truth,

it is actually privately owned… and that the “FED” actually has “reserves”

when it just prints more money as

debt that the U.S. taxpayers pay interest on. Has society discovered who

really owns the banks?

Is FED fraud a weapon of mass deception for fleecing the sheople?

Taxation without representation? Ya Think! – CR]